Business Valuation for Divorce: Understanding the Stakes Before You Agree

Your business represents years of hard work, sacrifice, and financial investment. When divorce enters the picture, that carefully built enterprise becomes one of the most contentious assets to divide. The process of determining what your business is actually worth can feel overwhelming, especially when emotions run high and financial futures hang in the balance.

Business owners face unique pressures during divorce. Nearly 43-48% of entrepreneurs experience divorce, a rate significantly higher than the general population. The stakes are considerable: 57% of business owners report their company suffering a financial hit during proceedings, with an average monthly revenue decline of $4,000.

Understanding how business valuation for divorce works isn’t just about protecting your financial interests. It’s about making informed decisions that shape your post-divorce life, whether you plan to keep the business, buy out your spouse, or explore other options. This guide walks you through every aspect of the process, from determining when you need professional help to navigating the challenges that commonly arise.

If you’re trying to make sense of what a business valuation could mean for your settlement and next steps, Even Path’s fiduciary process is designed to help you slow down and evaluate your options clearly before decisions become permanent.

TL;DR: Business Valuation for Divorce

Business valuation during divorce determines far more than a number. It shapes settlement options, support obligations, tax outcomes, and your ability to move forward without prolonged financial entanglement. Valuations can vary widely depending on methodology, assumptions, and state rules, especially when income, goodwill, or ownership structure is disputed. Understanding how valuation works, where it often goes wrong, and when professional guidance is necessary helps you avoid rushed decisions that create long-term financial stress. With clear, fiduciary guidance, it’s possible to slow the process down and make informed choices that protect both your financial future and your emotional well-being.

Key Points: Business Valuation for Divorce and the Decisions It Drives

- Business valuation directly affects settlement structure, support calculations, and long-term financial stability

- Different valuation methods can produce dramatically different outcomes for the same business

- Errors often come from hidden income, goodwill disputes, or using the wrong valuation approach

- Not every business requires a full appraisal, but skipping one carries long-term risk

- Post-valuation decisions like buyouts, asset trades, or continued ownership involve real tradeoffs, not just math

- Divorce-related valuations require coordination between legal, financial, and emotional considerations

- Even Path helps clients evaluate valuation outcomes through a fiduciary, divorce-informed lens focused on clarity, not pressure

Table of Contents

Toggle

Why Business Valuation Matters in Divorce

The value assigned to your business directly impacts how much you’ll pay or receive in your settlement. Courts treat businesses as assets that must be accounted for during property division, and the valuation figure becomes the foundation for all subsequent negotiations.

Getting the valuation right matters more than most people realize. An inflated value could force a business owner to liquidate other assets or take on debt to buy out their spouse’s interest. An undervalued business leaves the non-owner spouse with less than their fair share. Both scenarios create financial hardship and resentment that can last for years.

Marital vs. Separate Property: When Your Business Gets Divided

Whether your business qualifies as marital property depends largely on when you started it and how it grew during your marriage. A business you founded before marriage typically counts as separate property. However, any increase in value during the marriage often becomes subject to division.

The distinction gets murky when both spouses contributed to the business. Courts examine factors like whether the non-owner spouse helped with operations, provided financial support, or sacrificed career opportunities to support the business. Even indirect contributions, such as managing the household while the owner spouse built the company, can establish marital interest in the business.

Different states apply varying standards for dividing business assets. Community property states typically split marital assets 50/50, while equitable distribution states aim for fairness rather than equal division. The date of separation or filing also matters, as business value fluctuations between separation and trial can impact what gets divided.

How Business Value Impacts Your Settlement

The business valuation figure ripples through every aspect of your divorce settlement. A higher valuation means more assets to offset if one spouse keeps the business. It affects spousal support calculations, tax implications, and the overall distribution of marital property.

Consider Sarah, who owned a $500,000 marketing agency. She kept the business and offset Mark’s $250,000 share by trading him her 401(k) worth $180,000 plus $70,000 in home equity. The tax implications created real differences: Sarah’s business income remained taxable at ordinary rates, while Mark’s 401(k) transfer was tax-free under divorce rules but subject to future taxes on withdrawal. The after-tax value of their settlements differed by roughly $40,000.

Business value also influences support obligations. Courts look at the income-generating capacity demonstrated by the business when setting alimony or maintenance amounts. A thriving business suggests greater ability to pay support, while a struggling enterprise might result in lower support obligations.

This is often where people realize that understanding the number is only part of the equation. Interpreting how that value interacts with support, taxes, and long-term cash flow requires a broader financial lens than legal negotiations alone. Even Path works with clients at this stage to translate valuation outcomes into practical financial decisions that align with their post-divorce reality.

When You Need a Professional Business Valuation

Not every business in divorce requires a formal appraisal. Small side hustles with minimal revenue or businesses operating at a loss might not justify the cost and time of professional valuation. However, most established businesses benefit from expert assessment to ensure equitable division and protect both parties’ interests.

Scenarios That Require Formal Appraisal

Complex business structures or intricate operations demand professional valuation. Businesses with multiple revenue streams, intellectual property, trusts, holding companies, or significant involvement of both spouses present challenges that require expert assessment. The valuator must untangle assets, liabilities, and operational complexities to arrive at an accurate figure.

Discretionary expenses or non-disclosure concerns also necessitate professional help. Personal expenses disguised as business costs are common: luxury vehicles claimed as company assets, excessive family payroll, above-market rent paid to related entities. Suspicions of incomplete financial disclosure require forensic review and normalization adjustments that only trained experts can perform properly.

Company-specific risks make professional valuation essential. Customer concentration, owner dependency, short operating history, or uncertain future earnings require realistic projections beyond historical data. Experts quantify these risks through sensitivity analysis and apply appropriate adjustments to the valuation.

Significant profits, turnover, or asset discrepancies signal the need for formal appraisal. High profits mismatched with lifestyle, undervalued capital assets like property, or co-mingled marital funds mandate valuation to ensure accurate fair market value. Ownership complications add another layer: multiple shareholders, fluctuating value between separation and trial, or liquidity issues require professional methods to handle partial interests.

When You Might Skip Professional Valuation

Professional valuation costs money and takes time. Small businesses with straightforward finances and minimal value sometimes don’t warrant the expense. If both spouses agree on a ballpark figure and the business represents a minor portion of total marital assets, informal assessment might suffice.

Sole proprietorships operating from home with little equipment or inventory may not need formal appraisal. Similarly, if the business is clearly worth less than the cost of valuation itself, informal agreement makes more financial sense. Some couples successfully use tax returns and basic financial statements to reach consensus without hiring experts.

The risk of skipping professional valuation centers on future disputes. If either spouse later claims the agreed-upon value was unfair, reopening the case becomes costly and complicated. Courts generally respect formal valuations more than informal agreements, providing protection against future challenges.

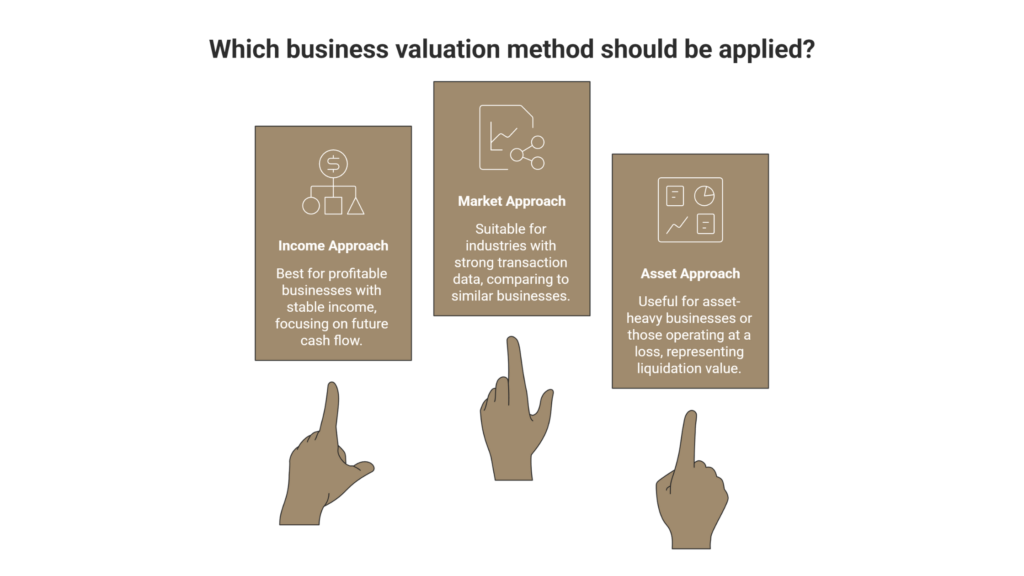

The Three Standard Business Valuation Approaches

Appraising a business relies on three established methodologies, each suited to different business types and circumstances. Valuators often apply multiple methods to cross-check results and build a defensible valuation. Understanding these approaches helps you anticipate what your valuator will examine and how they’ll reach their conclusions.

Consider a 15-year-old HVAC company with $800,000 annual revenue, $180,000 in net income, and $320,000 in equipment and inventory. The owners are divorcing, and three different methods produce strikingly different results:

Using the income approach and capitalizing normalized earnings of $180,000 at a 25% rate (reflecting industry risk and owner dependency), the valuator arrives at $720,000. This method focuses on the business’s ability to generate future cash flow for a new owner.

The market approach examines recent sales of similar HVAC companies. Database research shows businesses in this revenue range selling for 0.8-1.0 times revenue or 3.5-4.5 times EBITDA. Applying a conservative 0.85 revenue multiple yields $680,000, while a 4.0 EBITDA multiple produces $720,000. The valuator settles on $700,000 after considering company-specific factors.

The asset approach tallies tangible assets: $320,000 in equipment and inventory, $45,000 in receivables, less $80,000 in liabilities, resulting in $285,000 net asset value. This represents the floor value but ignores the company’s earning power and customer relationships.

The valuator reconciles these figures by weighting the income approach most heavily at 50% ($360,000), the market approach at 40% ($280,000), and the asset approach at 10% ($28,500), reaching a final opinion of value around $668,500. The asset approach receives less weight because this operating business derives value primarily from ongoing operations, not liquidation.

Valuation Approach | What It Focuses On | When It’s Most Appropriate | Key Limitation |

Income Approach | Future earning power and cash flow | Profitable businesses with stable or predictable income | Highly sensitive to assumptions about risk and future earnings |

Market Approach | Sale prices of comparable businesses | Industries with strong transaction data and comparable sales | Comparables may not reflect unique business risks or ownership structure |

Asset Approach | Net value of tangible and intangible assets | Asset-heavy businesses or companies operating at a loss | Often undervalues ongoing businesses by ignoring earning potential |

Income Approach: Valuing Based on Earnings

The income approach focuses on the business’s ability to generate future earnings. This method proves most effective for profitable businesses with predictable cash flow and reasonable growth projections. It treats the business as an investment, calculating what a buyer would pay based on expected returns.

Capitalization of Earnings Method

Capitalization of earnings converts expected future earnings into present value. The valuator analyzes historical earnings, normalizes them to reflect sustainable levels, and applies a capitalization rate that accounts for risk and expected return.

This method works well for stable businesses with consistent earnings. The valuator calculates maintainable earnings by adjusting for one-time events, discretionary expenses, and owner compensation that differs from market rates. The capitalization rate reflects industry risk, company-specific factors, and economic conditions. Higher risk or uncertainty increases the rate, which decreases the overall value.

Discounted Cash Flow (DCF) Method

DCF projects future cash flows for several years and discounts them to present value. This approach suits businesses experiencing growth, change, or irregular earnings patterns. The valuator builds financial projections, estimates terminal value at the end of the projection period, and applies a discount rate reflecting risk.

DCF requires more assumptions than capitalization of earnings, making it vulnerable to manipulation. Optimistic projections inflate value, while pessimistic forecasts deflate it. The discount rate selection significantly impacts results. Courts scrutinize DCF valuations carefully, requiring valuators to justify their assumptions with market data and business fundamentals.

Market Approach: Comparing to Similar Businesses

The market approach benchmarks your business against comparable companies that recently sold or are publicly traded. This method provides real-world validation of value based on what buyers actually pay for similar businesses. It works best when sufficient comparable data exists.

The guideline public company method compares your privately held business to publicly traded companies in the same industry. The valuator identifies several public companies with similar operations, size, and markets, then derives valuation multiples from their trading prices. Common multiples include price-to-earnings, price-to-revenue, and price-to-EBITDA ratios. Privately held businesses typically receive a discount compared to public companies due to lack of marketability.

The transaction method analyzes actual sales of comparable private businesses. Databases track business sales by industry, size, and location, providing multiples based on completed transactions. Industry multipliers provide rules of thumb for common business types. Restaurants might sell for 2-3 times annual revenue, while professional services firms trade at 0.5-1.5 times revenue. These multipliers serve as reality checks against other methods but shouldn’t be the sole basis for valuation.

Asset Approach: Net Asset Value Calculation

The asset approach calculates value based on the business’s net assets: total assets minus total liabilities. This method proves most useful for asset-heavy businesses, holding companies, or businesses operating at a loss. It provides a floor value representing what the business would be worth in liquidation.

The valuator adjusts balance sheet values to fair market value. Real estate gets appraised at current market rates rather than historical cost. Equipment and inventory are valued based on what they’d fetch in a sale. Intangible assets like customer lists, trademarks, or goodwill receive separate valuation.

This approach often undervalues profitable operating businesses because it doesn’t capture earning power. However, it provides a useful baseline and works well for businesses where assets drive value more than operations.

Which Valuation Method Applies to Your Business

Methods depend on your company’s characteristics. Service businesses with minimal assets and strong client relationships typically rely on income approaches. Manufacturing companies with significant equipment and inventory might use asset approaches supplemented by market comparisons.

Professional valuators often employ multiple methods and reconcile the results. Your industry, business model, profitability, growth trajectory, and available data all influence method selection. Businesses with unique characteristics or limited comparables might rely more heavily on income approaches, while those in industries with active transaction markets benefit from market-based methods.

The Business Valuation Process: What to Expect

Understanding the business valuation process helps you prepare effectively and avoid surprises. Experienced divorce business valuators follow systematic approaches to ensure thorough analysis and defensible conclusions. The process typically unfolds over several weeks to months, depending on complexity and court deadlines.

Step 1: Selecting and Hiring a Qualified Valuator

Choosing the right valuator sets the foundation for credible results. According to FAZ Forensics, finding an appraiser committed to the industry and holding credentials such as Accredited Senior Appraiser (ASA), Accredited in Business Valuation (ABV), Certified Valuation Analyst (CVA), or Certified Business Appraiser (CBA) is crucial. Look for professionals with recognized credentials and divorce-specific experience.

Both spouses sometimes hire separate experts, particularly in contentious cases. This approach provides each party with their own analysis but often leads to conflicting valuations that must be reconciled through negotiation or trial testimony. Joint experts save money and time but require both parties to trust one professional’s judgment.

Step 2: Document Gathering and Financial Review

Valuators need comprehensive financial information spanning 3-5 years. Tax returns form the foundation, supplemented by profit and loss statements, balance sheets, cash flow statements, and accounts receivable and payable aging reports. The valuator also requests operating agreements, shareholder agreements, and any buy-sell provisions.

Additional documents include customer contracts, lease agreements, equipment lists, loan documents, and intellectual property records. The valuator examines bank statements, credit card records, and checks for large or unusual transactions. Complete documentation enables thorough analysis and reduces the risk of overlooking important value drivers or red flags.

Step 3: Normalization Adjustments and Financial Analysis

Raw financial statements rarely reflect maintainable earnings. The valuator normalizes financials by adjusting for discretionary expenses, one-time events, above or below-market owner compensation, and personal expenses run through the business.

Take a dental practice that reported $120,000 in net income on its tax returns. After the valuator conducted normalization adjustments, the true earning power looked dramatically different:

- Owner salary adjustment: +$40,000 (was paying self $180,000; market rate for associate dentist is $140,000)

- Personal vehicle expenses: +$15,000 (luxury SUV lease used primarily for personal use)

- One-time legal costs: +$8,000 (lawsuit settlement unrelated to operations)

- Related-party rent adjustment: +$12,000 (paying sister $5,000/month for office space worth $4,000/month)

Normalized earnings: $195,000

This $75,000 difference translates to roughly $300,000 in additional business value using a 25% capitalization rate. The owner spouse argued the original $120,000 figure reflected true profitability, but the valuator’s analysis revealed the business could generate $195,000 in earnings for a typical buyer not running personal expenses through the company.

This analysis reveals the business’s true earning power and helps identify potential income manipulation. The valuator scrutinizes unusual expense patterns, inconsistencies between tax returns and books, and discrepancies between reported income and lifestyle.

Step 4: Applying Valuation Methods and Discounts

The valuator applies appropriate methods based on business characteristics and available data. They calculate value using selected approaches, then consider discounts or premiums based on specific factors affecting marketability and control.

Minority interest discounts reduce value when the spouse owns less than controlling interest. Lack of marketability discounts account for the difficulty of selling private company shares. However, courts like those in Massachusetts prohibit marketability discounts for non-sale scenarios, increasing assigned values despite real sale barriers.

Step 5: Receiving and Reviewing the Valuation Report

The final report documents the valuator’s methodology, analysis, and conclusions. It includes company background, financial analysis, valuation approaches applied, and the final opinion of value. Detailed reports also explain assumptions, limiting conditions, and reasoning behind major decisions.

Review the report carefully with your attorney. Question any assumptions that seem unrealistic or unfavorable. Understand the strengths and weaknesses of the valuation before negotiations or trial. If you hire your own expert, they’ll critique the opposing valuator’s report and identify areas of disagreement.

Timeline and Cost Considerations

Small to medium business valuations typically take a few weeks to several months. Complexity, court deadlines, and whether one or dual appraisals are needed affect timing. Initiating valuation early in the divorce process provides a benchmark and enables settlement discussions before litigation costs mount.

How much does a small business valuation cost? Expect to pay $4,000-$10,000 per valuation for straightforward cases. Complex businesses, dual reports, expert witness testimony, and litigation escalate costs significantly. Some valuations, particularly for larger businesses or those requiring extensive forensic analysis, can exceed $25,000-$50,000.

Investing in quality valuation often pays dividends. Accurate valuations facilitate fair settlements, reduce litigation costs, and provide defensible positions if disputes reach trial.

Critical Challenges in Divorce Business Valuation

Business and divorce cases present unique complications that can derail even straightforward valuations. Recognizing these challenges helps you address them proactively and protect your interests throughout the process.

Hidden Assets and Income Manipulation

Controlling spouses sometimes underreport revenue, inflate expenses, or conceal funds to reduce business value. Cash-intensive businesses face particular scrutiny since income can disappear without proper documentation. Forensic accountants look for red flags like declining revenue inconsistent with industry trends, excessive or unusual expenses, and lifestyle inconsistent with reported income.

Hidden assets or income concealment remains routine in contentious divorces. The valuator might subpoena bank records, interview employees, or review point-of-sale systems to verify reported income. Courts penalize fraud harshly when discovered, sometimes awarding the victimized spouse a larger share of assets or charging sanctions.

Expert Valuation Disputes: When Numbers Tell Different Stories

Competing valuations from spouse-hired experts can differ by hundreds of thousands of dollars based on methodological choices. In the 2024 UK case WW v XX, a private financial company faced dueling expert opinions that illustrated how assumptions drive outcomes. Both experts used earnings-based methods on the husband’s £2.4 million shareholding, but disagreed on the appropriate multiplier.

One expert’s multiplier produced a valuation around £15.6 million, while the other’s yielded approximately £10.4 million (a £5.2 million spread). The judge averaged the two approaches, arriving at roughly £9.98 million total value (including £1.89 million in property appreciation). Even after adjusting for the pre-marital portion (reduced from £1.25 million to £2.77 million net), the court determined £7.2 million represented matrimonial value subject to division.

The husband retained the business but paid the wife £2.5 million in installments over seven years, creating a 38:62 split that favored the husband. This case demonstrates how volatile profitability, cross-border assets, and expert disagreement over multipliers can create uncertainty that courts must resolve through compromise rather than precision.

The Double-Dipping Problem

Double-dipping occurs when the same income stream gets counted twice: once in business valuation and again in spousal support calculations. This creates unfair double recovery for the recipient spouse and excessive burden on the payor.

The issue typically arises when income-based valuation methods project future earnings. If those same earnings also determine support obligations, the payor effectively pays twice for the same income. States handle this differently. Some exclude personal goodwill from business value to avoid double-counting, while others reduce support to offset the overlap.

Addressing double-dipping requires careful coordination between business valuation and support calculations. Your attorney and valuator should explicitly consider this issue and structure recommendations to avoid unfair duplication.

Minority Interest and Marketability Discounts

Discount disputes frequently arise when one spouse owns partial interest in a business with other partners. Courts and experts disagree about whether and how much to discount minority interests for lack of control and difficulty finding buyers.

Valuation disagreements arise frequently due to differing methods and discount applications. Some jurisdictions prohibit certain discounts in divorce cases, reasoning that the business isn’t actually being sold and the marital estate shouldn’t bear those costs. Other courts apply standard discounts as they would in any business transaction.

Goodwill: Personal vs. Enterprise Value

Goodwill represents value beyond tangible assets and measurable cash flows. Enterprise goodwill attaches to the business itself and transfers to new owners. Personal goodwill reflects the owner’s individual reputation, skills, and relationships and doesn’t transfer.

Distinguishing between personal and enterprise goodwill becomes critical in professional practices and personal services businesses. A surgeon’s practice derives much value from their personal reputation, while a dental practice with multiple practitioners has more enterprise goodwill. Only enterprise goodwill typically counts as a divisible marital asset.

Courts scrutinize goodwill valuations closely, particularly when excluding personal goodwill might dramatically reduce business value. Expert testimony and careful analysis of what drives business value help establish appropriate treatment.

Top Mistakes in Business Valuation and How to Avoid Them

According to valuators and family law practitioners, several recurring errors undermine the accuracy and fairness of divorce business valuations. Understanding these pitfalls helps both business owners and non-owner spouses protect their interests.

Using the Wrong Valuation Method

Fair market value and discounted future earnings are frequently misused. Family law firm Feinberg & Waller notes: Often, fair market value and discounted future earnings are not appropriate methods to calculate the value of a business interest in divorce. First, privately held companies are usually illiquid… Second, discounted future earnings are usually never appropriate because community property can only be acquired during the course of the marriage.

Business owners typically push asset-based approaches that undervalue service firms’ income potential, while non-owners overlook goodwill. Both spouses should insist on multiple methods reconciled by credentialed appraisers to capture intangibles like goodwill without speculation.

Failure to Include All Assets and Liabilities

Overlooking cash, equipment, accounts payable, or intangibles skews results. Feinberg & Waller warns: Failure to include all the assets and liabilities of the business… many significant assets and liabilities often go overlooked… may focus on the value of the business’ goodwill and fail to include cash on hand, office equipment, or accounts payable.

Mandate forensic evaluators to compile exhaustive balance sheets, including tangibles and intangibles like patents. Non-owners undervalue by ignoring hidden liabilities; owners hide assets to reduce their buyout obligations.

Hiring Unqualified or Biased Experts

Part-time CPAs or generalists lack divorce-specific expertise, leading to rejected valuations in court. McNees Wallace & Nurick emphasizes the need for Certified Business Appraisers, Accredited Senior Appraisers (ASA), or CPAs skilled at analyzing cash flow.

Each spouse must retain an independent, credentialed expert experienced in family law and the industry. The 2025 UK case DF v YB illustrates this principle. The husband’s accountant valued his special purpose vehicle holding (shares, loan notes, and directors’ loan account) at £460,257. The wife challenged this figure, proposing £640,453, but provided no supporting expert evidence of her own.

The court adopted the husband’s figures, deeming the wife’s challenges “unsatisfactory” and impossible to verify without counter-evidence. Even in this high-cost dispute totaling £945,000 in legal fees, the court ordered equal division of £14.2 million net assets with a £510,000 lump sum to the wife. The lesson: challenges to expert valuations require your own qualified expert, or courts default to the evidenced side.

Ignoring Unique Events, Risks, or Valuation Dates

Using peak earnings without adjustments or wrong dates distorts value significantly. Feinberg & Waller states: Failure to adjust for unique events and risks… your business may have been awarded a one-time contract… there is more risk involved in running certain types of businesses.

Experts should normalize financials for anomalies and use court-specified dates. Business owners often inflate value with one-off gains, while non-owners ignore growth risks.

Your Options After Business Valuation

Once you know what your business is worth, you face decisions about how to handle this asset in your divorce settlement. Each option carries different financial, operational, and emotional implications.

Buyout: One Spouse Keeps the Business

The most common solution involves one spouse retaining the business and buying out the other’s interest. This provides clean separation and allows the business to continue without divided ownership complications. The buyout spouse typically receives cash, other marital assets, or a combination to offset the business value.

Buyouts require sufficient assets or financing to fund the payment. If you lack liquid assets, you might need to refinance the business, secure loans, or structure payment terms over several years. Tax implications of different asset trades significantly impact the real value each spouse receives.

Business divorce cases like Martin v. Abrams show how disputes over buyout terms can lead to prolonged litigation when parties can’t agree on valuation or payment structure. Clear agreements and realistic expectations facilitate smoother buyouts.

Continued Co-Ownership Arrangements

Some divorcing spouses maintain business co-ownership post-divorce. This works best when both parties actively participate in operations, can maintain professional working relationships, and agree on business strategy. Co-ownership requires detailed agreements governing management authority, profit distribution, and future exit mechanisms.

Continued co-ownership carries significant risks. Personal conflicts can spill into business decisions, damaging operations and value. One spouse might sabotage the business or create conflicts with employees and customers. Clear operating agreements with dispute resolution mechanisms help manage these risks but can’t eliminate them.

Selling the Business and Splitting Proceeds

Selling the business and dividing the proceeds provides certainty and liquidity. Both spouses get cash rather than dealing with ongoing business entanglements. This option appeals when neither wants to retain ownership or when buyout financing isn’t feasible.

Business sales take time and may not fetch the appraised value, particularly in forced sale situations. Marketing the business during divorce proceedings can disrupt operations and spook customers or employees. Some business buyers exploit divorce situations, offering below-market prices knowing sellers face pressure to close quickly.

Nearly 5% of business owners close their doors due to divorce’s financial burden. Avoiding forced closure or fire-sale prices requires careful planning and realistic timelines.

Trading the Business for Other Assets

Asset offsets allow one spouse to keep the business while the other receives equivalent value in different assets. The business owner might trade home equity, retirement accounts, investment portfolios, or other property to balance the settlement.

This approach requires sufficient other assets to offset business value. It also demands careful attention to tax implications. Trading a business worth $500,000 for retirement accounts of equal value may not provide equal after-tax value. Work with financial advisors to structure trades that account for tax consequences and liquidity differences.

Protecting Your Interests During Valuation

Business valuation and divorce proceedings demand active participation and vigilance from both spouses. Taking steps to protect your interests throughout the process helps ensure fair outcomes.

If You’re the Business Owner Spouse

Maintain transparent, complete financial records and be prepared for scrutiny. Attempting to hide assets or manipulate income typically backfires when discovered, damaging your credibility and potentially resulting in sanctions. Focus on demonstrating legitimate business expenses and normal financial practices.

Prioritize business continuity by shielding divorce conflicts from employees, customers, and competitors. Operational disruption reduces value for both parties. About 70% of business owners report being unable to focus on work during divorce, which directly impacts revenue and profitability.

Engage experienced valuation experts early who understand both your industry and divorce-specific issues. Generic business appraisers may lack familiarity with marital property law and valuation standards courts apply in divorce cases. Consider hiring your own expert rather than relying solely on a court-appointed valuator, particularly if significant value is at stake.

If You’re the Non-Owner Spouse

Actively seek full financial disclosure rather than accepting limited information. Request copies of all business records, tax returns, and financial statements. If you suspect undervaluation or hidden income, push for forensic accounting review.

Hire your own business valuation attorney or financial expert to review information and protect your interests. Don’t assume the other spouse’s valuator or a jointly appointed expert fully represents your position. Independent analysis provides leverage in negotiations and credibility if the case proceeds to trial.

Question valuations that seem inconsistent with the lifestyle the business supported during marriage. If the business “suddenly” became less profitable after divorce filing, investigate whether real business decline occurred or whether income manipulation is occurring.

Red Flags That Suggest Improper Valuation

Watch for revenue declines that coincide suspiciously with divorce filing; new expenses that can’t be explained or verified; and customer or vendor relationships shifting to entities controlled solely by the business owner spouse. Dramatic changes in owner compensation or distributions, reluctance to provide complete financial documentation, and unusual accounting changes or method switches also warrant scrutiny.

Valuations significantly lower than industry benchmarks or prior business appraisals signal potential problems. If your spouse suddenly claims the business has minimal value despite years of comfortable lifestyle, dig deeper with professional help.

How to Choose the Right Business Valuator

Selecting a qualified valuator significantly impacts the credibility and defensibility of your business valuation. The wrong choice can cost you money through inaccurate valuations or additional litigation to resolve disputes.

Required Credentials and Qualifications

Look for valuators holding recognized professional certifications. The Accredited Senior Appraiser (ASA) designation from the American Society of Appraisers requires a college degree, at least three years of full-time business valuation experience, passing written examinations, and submission of appraisal reports for peer review.

The Certified Valuation Analyst (CVA) credential from the National Association of Certified Valuation Analysts requires CPA status, completion of coursework, examinations, and case study submission. The Accredited in Business Valuation (ABV) designation from the AICPA builds on CPA credentials with specialized business valuation training and experience.

These credentials ensure the valuator understands professional standards, maintains independence, and follows systematic valuation methodologies. Courts respect credentialed experts more than general business consultants without formal valuation training.

Questions to Ask Before Hiring

Interview potential valuators about their experience and approach. Ask how many divorce valuations they’ve completed, what percentage of their practice involves family law cases, and whether they’ve testified as expert witnesses in court. Inquire about their familiarity with your specific industry and business type.

Discuss their typical methodology and timeline for completing valuations. Ask about their fee structure, whether they charge hourly or flat rates, and what cost range you should expect. Question how they handle disagreements with opposing experts and their approach to defending their conclusions.

Request references from attorneys who’ve worked with the valuator in divorce cases. Check whether any complaints or disciplinary actions exist against them with professional organizations. Verify their credentials and continuing education compliance.

Joint Expert vs. Separate Experts

Deciding whether to hire a joint expert or separate experts depends on your case dynamics and relationship with your spouse. Joint experts cost less, produce one valuation both parties accept, and streamline the process. They work when both spouses trust the selected professional and maintain reasonably amicable relations.

Separate experts make sense in contentious cases, when significant assets are at stake, or when you suspect the other spouse might manipulate information. Having your own expert provides independent analysis, someone who advocates for your position, and ability to critique the opposing expert’s conclusions.

The downside of separate experts involves higher costs and likely need for testimony at trial when valuations differ. Valuation disagreements arise frequently due to differing methods and assumptions, requiring judges to weigh competing expert testimony.

Preparing for Your Business Valuation

Thorough preparation streamlines the valuation process and helps ensure accurate results. Taking steps before the valuator begins work demonstrates good faith and provides the foundation for credible analysis.

Essential Documents to Gather

Compile comprehensive financial documentation spanning multiple years. Core documents include tax returns for the past 3-5 years, balance sheets, profit and loss statements, cash flow statements, and general ledgers. Include both business and personal tax returns since business income often flows to personal returns.

Gather operational documents like business formation papers, shareholder or operating agreements, buy-sell agreements, and any amendments. Include customer contracts, supplier agreements, lease documents, and loan agreements. Compile lists of business assets including equipment, real estate, intellectual property, and inventory.

Prepare records showing accounts receivable and payable, bank statements, credit card statements, and cancelled checks for unusual or large transactions. Document any business debts, lines of credit, or contingent liabilities. If the business owns real estate or significant equipment, obtain recent appraisals or valuations.

Steps to Take Before the Process Begins

Review financial records for accuracy and completeness before submitting them to the valuator. Identify and gather documentation for any unusual transactions, one-time events, or anomalies that might require explanation. This proactive approach prevents delays and demonstrates credibility.

Consider conducting a preliminary review with a forensic accountant if you’re the non-owner spouse or if you suspect financial irregularities. This helps identify red flags and areas requiring deeper investigation before formal valuation begins.

If you’re the business owner, ensure your books are current and properly maintained. Address any accounting irregularities or documentation gaps. Organize records logically to facilitate the valuator’s review. Being organized and responsive speeds the process and reduces costs.

Conclusion

Coordinate closely between your attorney and valuator throughout the process. Your attorney understands the legal requirements and standards courts apply, while the valuator handles technical financial analysis. Communication between these professionals ensures the valuation addresses relevant legal issues and provides information courts need.

Be responsive to document requests and information inquiries from your valuator. Delays in providing records extend the timeline and increase costs. Answer questions honestly and completely, even if the information seems unfavorable. Attempting to hide or misrepresent information damages your credibility and can result in worse outcomes.

Understand that business valuation involves both science and judgment. Valuators make assumptions and apply professional judgment in areas where exact answers don’t exist. Reasonable experts can reach different conclusions using the same data. Focus on ensuring your valuator has complete, accurate information and understands the specific factors affecting your business.

The national divorce rate approaches 50%, making business valuation a critical concern for many entrepreneurs and professionals. Whether you’re navigating how to value a business for divorce for the first time or dealing with complex valuation disputes, understanding the process helps you make informed decisions and protect your financial future.

Quality preparation, selecting qualified professionals, and maintaining realistic expectations about business value help you negotiate this challenging aspect of divorce. The business you built deserves careful, professional assessment that leads to fair resolution for both spouses while preserving value and enabling both parties to move forward successfully.

If you’re ready to talk through your situation and understand your options, you can schedule a confidential conversation here.