Pre Retirement Anxiety: 7 Proven Ways to Feel Confident

Understanding social security spousal benefits divorce rules can feel overwhelming when you’re navigating separation. The financial decisions you make now about claiming benefits on your ex-spouse’s record can impact your retirement security for decades, yet many people rush through these choices without fully understanding the permanent trade-offs involved.

Divorced spouse benefits exist specifically to provide financial stability after a significant marriage ends. Whether you’re approaching retirement age or planning years ahead, knowing your options helps you make clear-headed decisions during an inherently stressful transition. Even Path specializes in helping individuals navigate these emotionally complex financial decisions, offering guidance that prioritizes clarity over urgency when permanent choices are at stake.

TL;DR: Social Security Spousal Benefits Divorce Guide 2026

If you were married for at least 10 years and are now divorced, you may qualify to receive up to 50% of your ex-spouse’s Social Security benefit without affecting what they receive. You must be at least 62, currently unmarried, and your ex-spouse must be eligible for benefits (though they don’t need to have filed yet). The amount you receive depends on when you claim, with early claiming at 62 resulting in permanently reduced payments compared to waiting until your full retirement age. Your ex-spouse won’t be notified when you apply, and their remarriage doesn’t impact your eligibility. Understanding these rules and strategically timing your claim can significantly affect your long-term financial security.

Key Points

- Marriage duration is non-negotiable: The 10-year marriage requirement is strictly enforced, with no exceptions for shorter marriages regardless of economic circumstances during the relationship.

- Privacy is protected: Your ex-spouse receives no notification when you claim benefits on their record, eliminating concerns about unwanted contact or judgment.

- Early claiming carries permanent consequences: Claiming before full retirement age results in a reduced benefit that never increases, making the timing decision particularly critical.

- Remarriage changes everything: Getting remarried typically ends your eligibility for benefits on your ex’s record, though exceptions exist for remarriage after age 60 in survivor benefit situations.

- Your claim doesn’t affect your ex: The benefits you receive come from the Social Security system, not from your ex-spouse’s individual payments, allowing you to claim without guilt or concern about reducing their income.

- Timing strategies require personalized analysis: Break-even calculations, longevity considerations, and work history comparisons demand individualized planning rather than one-size-fits-all advice.

- Documentation requirements are specific: Gathering marriage certificates, divorce decrees, and personal identification documents before applying prevents frustrating delays in receiving benefits.

Table of Contents

Toggle

What Are Divorced Spouse Social Security Benefits?

Divorced spouse Social Security benefits provide income protection for individuals whose marriages lasted long enough to create economic interdependence but ended before retirement. The system recognizes that long-term partners who may have sacrificed career advancement for family responsibilities deserve benefits even when marriages don’t last.

Approximately 489,000 divorced individuals aged 62 or older receive benefits based on their ex-spouse’s earnings record. Women comprise 95% of recipients of spousal or survivor benefits on divorced partners’ records, reflecting historical workforce participation patterns and the protective purpose these benefits serve.

How Divorced Spouse Benefits Work

The structure mirrors married spousal benefits in most respects. You can receive up to 50% of your ex-spouse’s primary insurance amount when you claim at your full retirement age, provided this amount exceeds your own retirement benefit. Social Security automatically calculates both amounts and pays you the higher of the two.

Your benefit calculation uses your ex-spouse’s earnings record exactly as if you were still married, drawing from their work history and contribution levels over their career. The system makes no distinction between current spouses and qualified ex-spouses when determining benefit amounts.

The key difference from married spousal benefits involves the independence of your claim. After being divorced for at least two years, you can claim benefits even if your ex-spouse hasn’t filed for their own retirement yet. This independence provides flexibility that married spouses don’t have, eliminating the need to coordinate timing decisions with your former partner.

Social Security maintains strict confidentiality regarding divorced spouse benefit claims. Your ex-spouse receives no notification when you apply, no updates about your benefit amount, and no ongoing communication about your claim status. This privacy protection removes a significant emotional barrier for many people considering whether to claim benefits on an ex’s record.

Your decision to claim divorced spouse benefits has zero impact on your ex-spouse’s Social Security payments. They receive the full amount they’re entitled to based on their work record, regardless of whether you claim benefits, when you claim them, or how much you receive. The misconception that claiming somehow “takes away” from an ex-spouse’s benefits prevents many eligible individuals from pursuing what they’ve earned through years of partnership. Your ex-spouse’s current spouse, if they’ve remarried, also faces no reduction in their potential spousal benefits due to your claim.

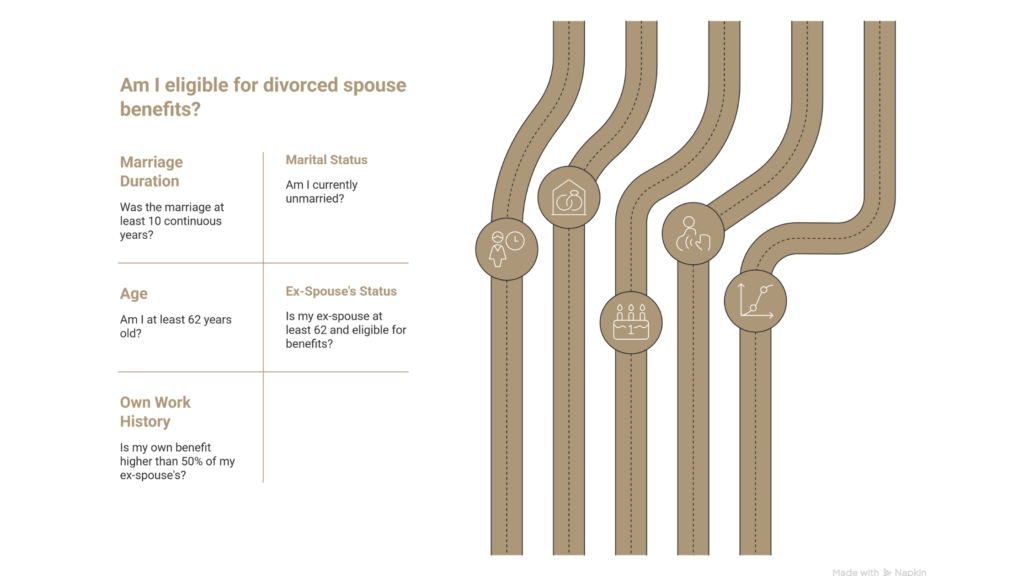

Eligibility Requirements for Divorced Spouse Benefits

Meeting eligibility requirements involves satisfying several distinct criteria, each serving a specific purpose in the benefit structure. These requirements ensure that benefits flow to individuals who had genuine long-term marital relationships and current financial need.

Marriage Duration Requirement

The foundation of eligibility rests on a marriage that lasted at least 10 continuous years. This duration reflects Congress’s determination that a decade represents sufficient time for economic interdependence to develop between partners. The median marriage duration for divorced spousal beneficiaries was 20 years, showing that most beneficiaries substantially exceed the minimum requirement.

The 10-year rule is strictly enforced without exceptions. Marriages lasting 9 years and 11 months don’t qualify, regardless of economic circumstances or hardship. If you remarried the same person, Social Security may combine continuous marriage periods to meet the threshold, but gaps between marriages to the same individual typically don’t count toward the requirement.

Current Marital Status Rules

You must be unmarried when you apply for and receive divorced spouse benefits. Remarriage generally terminates your eligibility to claim on your ex-spouse’s record, shifting your potential benefits to your new spouse’s work history instead.

Important exceptions exist for survivor benefits if you remarry after age 60 (or age 50 if disabled), but these exceptions don’t apply to standard divorced spouse retirement benefits. If your subsequent marriage ends through death, divorce, or annulment, your eligibility to claim on your first ex-spouse’s record can be restored.

Age Requirements for Claiming

You must be at least 62 years old to claim divorced spouse benefits, aligning with the minimum age for claiming retirement benefits generally. This age threshold represents the earliest point at which Social Security provides retirement income support, though claiming this early comes with permanent reductions in your monthly benefit amount.

Your full retirement age varies based on your birth year, ranging from 66 for those born before 1955 to 67 for those born in 1960 or later. Understanding your specific full retirement age is critical for evaluating the trade-offs between early claiming and waiting for unreduced benefits.

Your Ex-Spouse’s Status Requirements

Your ex-spouse must be at least 62 and eligible for Social Security retirement or disability benefits for you to qualify, but they don’t need to have actually filed for benefits. This eligibility requirement ensures that the work record you’re claiming against actually qualifies for benefits under Social Security rules.

If your ex-spouse hasn’t filed for their benefits yet and you’ve been divorced for less than two years, you must wait until the two-year post-divorce mark to claim. However, if your ex-spouse is already receiving retirement benefits, you can claim immediately upon reaching age 62 yourself, regardless of how long you’ve been divorced.

Your Own Work History Considerations

Your work history directly impacts the benefit amount you receive through the divorced spouse program. Social Security compares your own retirement benefit (based on your earnings record) with the divorced spouse benefit (based on your ex’s record) and pays you the higher amount.

If your own retirement benefit exceeds 50% of your ex-spouse’s primary insurance amount, you’ll receive your own benefit instead. This comparison happens automatically, but understanding where you stand before applying helps set realistic expectations.

How Much Can You Receive from Your Ex-Spouse’s Social Security?

The amount you can receive as a divorced spouse depends on multiple factors, including your ex-spouse’s earnings history, the age at which you claim, and whether you receive other government pensions. Understanding these factors helps you develop realistic expectations and make informed timing decisions.

Base Benefit Calculation Formula

At your full retirement age, you can receive up to 50% of your ex-spouse’s primary insurance amount. The primary insurance amount represents the benefit your ex-spouse would receive if they claimed at their full retirement age, calculated based on their lifetime earnings record.

As of November 2024, divorced spousal benefits average $909 per month. This average masks significant variation based on individual circumstances, with some divorced spouses receiving substantially more or less depending on their ex-spouse’s earnings history.

To illustrate with a concrete example, if your ex-spouse’s primary insurance amount is $4,000 per month, you could receive up to $1,000 monthly by claiming at your full retirement age. However, claiming at age 62 reduces this amount by roughly 30% to around $700, a reduction that never recovers.

Factors That Affect Your Benefit Amount

Several variables influence your actual benefit amount beyond the base calculation. Understanding these factors helps you anticipate what you’ll receive and plan accordingly for retirement income needs.

Early vs. Full Retirement Age Claiming

The age at which you claim divorced spouse benefits dramatically affects your monthly payment. Claiming before your full retirement age triggers permanent reductions calculated using a specific formula. For the first 36 months before your full retirement age, your benefit reduces by 25/36 of one percent for each month of early claiming. Beyond 36 months, an additional reduction of 5/12 of one percent applies for every month exceeding 36 months.

If your full retirement age is 67 and you claim at 62, you’re claiming 60 months early. This can reduce your potential benefit by roughly 30% compared to waiting until full retirement age. That reduction lasts for the rest of your life, making the decision to claim early one with permanent consequences.

Conversely, delaying your claim beyond full retirement age doesn’t increase divorced spouse benefits. Unlike your own retirement benefit, which grows by approximately 8% per year through delayed retirement credits until age 70, divorced spouse benefits max out at your full retirement age. This creates a clear strategic ceiling: there’s no financial advantage to waiting beyond your full retirement age to claim divorced spouse benefits.

Government Pension Offset (GPO)

If you receive a pension from government employment where you didn’t pay Social Security taxes, the Government Pension Offset may reduce your divorced spouse benefits. This offset exists to prevent “double-dipping” from government pension systems and Social Security spousal benefits.

The offset reduces your Social Security benefit by two-thirds of your government pension amount. For example, if you receive a $900 monthly government pension, your Social Security divorced spouse benefit would be reduced by $600. If this offset exceeds your potential divorced spouse benefit, you may receive no benefit at all despite meeting all other eligibility requirements.

Comparing Your Own Benefit vs. Ex-Spouse Benefit

One of the most important analyses in divorced spouse benefit planning involves comparing what you’d receive based on your own work record versus what you’d receive based on your ex-spouse’s record. Social Security makes this comparison automatically, but understanding the dynamics helps you plan strategically.

Your own retirement benefit is based on your personal earnings history over your highest 35 earning years. If you took significant time away from the workforce during your marriage, had lower-paying employment, or worked part-time to manage family responsibilities, your own benefit may be substantially lower than the divorced spouse benefit available through your ex’s record.

The system pays you the higher of the two amounts, effectively “topping up” your own benefit to reach 50% of your ex-spouse’s primary insurance amount if your personal benefit falls short. You receive your own benefit plus any additional amount needed to reach the divorced spouse benefit level. This structure ensures you always receive the maximum benefit available to you.

Real-World Scenarios: Claiming Decisions in Action

Understanding how abstract rules translate to actual financial impact requires examining specific situations with complete dollar calculations. These scenarios, based on realistic 2025 benefit levels and Social Security Administration rules, illustrate the trade-offs different claiming strategies create over a typical retirement span.

Case 1: Non-Working Ex-Spouse Claims at 62

Profile: Age 62 in 2023 (divorced 2021 after 15 years), no own earnings history (own benefit $0), ex-spouse’s primary insurance amount $3,000; no work post-claim.

Monthly benefit: 50% of $3,000 = $1,500 at full retirement age, reduced approximately 35% to $975 at age 62.

Income impact: $975/month × 12 = $11,700/year initially. Over 20 years (to age 82), cumulative benefits reach approximately $312,000 (excluding cost-of-living adjustments for simplicity). Claiming at full retirement age (67) would yield $1,500/month but only approximately $270,000 cumulative (5 fewer years of payments), so early claiming boosts total by roughly 16% despite the permanent monthly reduction.

Decision rationale: Early claiming suited her immediate financial needs and health concerns suggesting longevity below the break-even age of approximately 79. The certainty of current income outweighed the uncertainty of living long enough to benefit from higher future payments.

Case 2: Part-Time Worker Claims at Full Retirement Age 67

Profile: Age 67 in 2025 (divorced 2022 after 12 years), part-time work history yields own primary insurance amount $1,200; ex-spouse’s primary insurance amount $3,000; continues low earnings below annual limit (no reduction).

Monthly benefit: Own $1,200 + spousal excess ($1,500 – $1,200 = $300) = $1,500 total.

Income impact: $1,500/month × 12 = $18,000/year. Over 15 years (to age 82), cumulative benefits reach approximately $324,000. Claiming own benefit at 62 ($780 reduced) plus spousal at 62 would total approximately $1,105/month initially (approximately $199,000 cumulative), reducing lifetime benefits by roughly 39%. Waiting until full retirement age optimized her benefit given her work record and expected longevity.

Decision rationale: Continuing part-time work while delaying claiming until full retirement age maximized her monthly benefit without triggering earnings limits, providing optimal income security for her expected lifespan.

Case 3: Survivor-Divorced Claims at 62 After Ex’s Death

Profile: Age 62 in 2025 (divorced 2020 after 14 years), own primary insurance amount $900; ex-spouse died 2024 with primary insurance amount $2,800; no remarriage.

Monthly benefit: Survivor 100% of $2,800 reduced approximately 28% (earlier full retirement age for survivors) to $2,016 (versus spousal benefit of $1,400 if still alive).

Income impact: $2,016/month × 12 = $24,192/year. Over 20 years, approximately $580,000 cumulative. Delaying to full retirement age for full $2,800 would yield approximately $504,000 (13% less due to missed years). Early claiming proved ideal for immediate post-death income needs.

Decision rationale: The substantially higher survivor benefit compared to her own benefit, combined with immediate financial needs following her ex-spouse’s death, made early claiming the optimal choice despite the reduction from full retirement age claiming.

Case 4: Full-Career Worker Delays Own Benefit

Profile: Age 67 in 2025 (divorced 2023 after 11 years), strong career own primary insurance amount $2,200 (grows to $2,640 at age 70 with delayed credits); ex-spouse’s primary insurance amount $3,200; retires fully at 67.

Monthly benefit: Claims divorced spouse benefit $1,600 (50% of $3,200) at age 67, then switches to own delayed benefit $2,640 at age 70.

Income impact: Ages 67-69: divorced spouse benefit provides $1,600/month (approximately $57,600 cumulative over 3 years). Ages 70-82: own delayed benefit provides $2,640/month (approximately $380,160 cumulative over 12 years). Total lifetime benefits approximately $437,760. Pure divorced spouse strategy (claiming $1,600 at 67 through age 82) would yield approximately $288,000, making the delayed personal benefit strategy superior by approximately $150,000.

Decision rationale: Her strong earnings record made delaying her own benefit until age 70 optimal, while claiming the divorced spouse benefit at full retirement age provided income during the delay period. This strategic coordination maximized lifetime benefits given her financial resources and expected longevity.

These cases demonstrate that early claiming suits urgent cash needs or longevity concerns but cuts monthly amounts permanently; full retirement age or later maximizes monthly payments for longer lifespans. The optimal strategy depends on your specific health, financial resources, work history, and personal circumstances.

When Should You Claim Divorced Spouse Benefits?

Timing your divorced spouse benefit claim represents one of the most consequential decisions in your retirement planning. The permanent nature of the claiming age impact means this decision deserves careful analysis rather than rushed judgment.

Full Retirement Age by Birth Year (2026)

Your full retirement age determines when you can claim unreduced benefits and serves as the baseline for calculating early claiming reductions. For individuals planning their 2026 claiming strategy, understanding your specific full retirement age based on birth year is essential.

If you were born in 1960 or later, your full retirement age is 67. For those born between 1955 and 1959, full retirement age gradually increases from 66 and 2 months to 66 and 10 months, depending on your specific birth year. Those born in 1954 or earlier have already reached their full retirement age of 66 or earlier.

Knowing your full retirement age helps you calculate exactly how many months of early claiming reduction you’d face by claiming at any given age.

Understanding Break-Even Age: A Complete Example

The break-even age represents the point at which cumulative benefits from waiting to full retirement age surpass cumulative benefits from early claiming. Understanding this calculation helps you make informed decisions about timing.

Assumptions for this example:

- Ex-spouse’s primary insurance amount: $4,000/month

- Your divorced spouse benefit at full retirement age (67): $1,000/month (50%)

- Your reduced benefit at age 62: $700/month (30% reduction)

Cumulative value by age:

Age 67: Early claiming = $700 × 60 months = $42,000 | Waiting = $0

Age 75: Early claiming = $700 × 156 months = $109,200 | Waiting = $1,000 × 96 months = $96,000

Age 77: Early claiming = $700 × 180 months = $126,000 | Waiting = $1,000 × 120 months = $120,000

Age 79: Early claiming = $700 × 204 months = $142,800 | Waiting = $1,000 × 144 months = $144,000

Break-even age: Approximately 78 years, 10 months

Interpretation: If you live beyond age 79, waiting until full retirement age provides more lifetime income. If you have significant health concerns suggesting a lifespan shorter than 79, or urgent financial needs, early claiming may make sense despite the reduction.

Important considerations beyond break-even:

- This calculation doesn’t account for investment returns if you invest early benefits

- Inflation affects the relative value of early versus later dollars (though cost-of-living adjustments apply to both)

- Tax implications may favor one strategy depending on your total income picture

- The certainty of current income versus uncertainty of future longevity is a personal risk tolerance question

This detailed analysis demonstrates why claiming decisions require personalized evaluation. The “right” answer depends on your health, financial resources, other income sources, and comfort with uncertainty about future longevity.

Early Claiming: Pros and Cons

Claiming divorced spouse benefits at age 62, the earliest possible age, provides immediate income but comes with significant long-term costs. The permanent reduction in monthly benefits can amount to thousands of dollars over a retirement that might span 25 or 30 years.

The primary advantage of early claiming centers on immediate financial need. If you’re unable to work, lack other income sources, or face pressing financial obligations, accessing benefits at 62 might be necessary despite the reduced amount. Early claiming also makes sense if you have serious health concerns that suggest a shorter lifespan, as the reduced monthly benefit might deliver more total lifetime value than waiting for a higher payment you might not live long enough to benefit from.

The disadvantages compound over time. Beyond the permanent reduction in monthly income, early claiming while still working can trigger earnings limits that further reduce your benefits. For 2025 planning that extends into 2026, the earnings limit for individuals under full retirement age stands at $23,400 annually, with $1 withheld for every $2 earned above this threshold.

Delayed Claiming Considerations

Unlike your own retirement benefit, divorced spouse benefits don’t increase if you delay claiming beyond your full retirement age. This creates a clear strategic endpoint: once you reach full retirement age, there’s no financial incentive to wait longer to claim divorced spouse benefits.

However, if your own retirement benefit is close to or might exceed 50% of your ex-spouse’s primary insurance amount, delaying your claim could be advantageous. Your own benefit continues growing through delayed retirement credits until age 70, increasing by roughly 8% per year. If this growth would eventually make your own benefit larger than the divorced spouse benefit, strategic delay makes financial sense.

This scenario requires careful analysis comparing your projected own benefit at various claiming ages against the divorced spouse benefit available at your full retirement age.

Strategic Timing If You’re Still Working

Continuing to work while claiming divorced spouse benefits introduces additional considerations around earnings limits and benefit reductions. Understanding these interactions prevents costly surprises and helps optimize your overall financial picture.

If you’re under full retirement age and earning above the annual limit, Social Security withholds a portion of your benefits. For 2025 extending into 2026, this means $1 withheld for every $2 earned above $23,400 annually if you’re not reaching full retirement age during the year. In the year you reach full retirement age, the limit increases to $62,160 with $1 withheld for every $3 earned above this threshold.

These withheld benefits aren’t permanently lost. Once you reach full retirement age, Social Security recalculates your benefit to account for months when benefits were withheld, slightly increasing your ongoing monthly amount. However, this recalculation doesn’t fully compensate for the complexity and reduced cash flow during your working years.

Working also continues building your own earnings record, potentially increasing your own retirement benefit. If additional work years replace lower-earning years in your top 35 earning years calculation, your own benefit grows. This growth might eventually make your own benefit exceed the divorced spouse benefit.

How to Apply for Divorced Spouse Social Security Benefits

The application process for divorced spouse benefits is straightforward once you understand the required steps and documentation. Being prepared streamlines the process and helps you avoid frustrating delays in accessing your benefits.

When to Start Your Application

You can apply for benefits up to four months before you want your benefits to begin, but not earlier. This advance application window allows Social Security time to process your claim and verify your information before your desired start date. Applying within this timeframe helps ensure your first payment arrives promptly.

Starting your application before age 62 isn’t possible for divorced spouse benefits, as the minimum claiming age represents a hard eligibility threshold. However, planning ahead by gathering required documents and understanding your expected benefit amount helps you make informed decisions about the optimal claiming age for your circumstances.

Three Ways to Apply

Social Security offers three distinct application methods, each with specific advantages depending on your preferences and circumstances.

Applying online through your “my Social Security” account offers convenience and allows you to complete the application at your own pace. This method works well if you have all required documentation ready and feel comfortable navigating online forms. The system saves your progress, allowing you to return and complete sections over multiple sessions if needed.

Applying by phone through the national toll-free number at 1-800-772-1213 (TTY: 1-800-325-0778) provides the advantage of speaking with a representative who can answer questions and help guide you through the process. Representatives can clarify confusing aspects of your situation and help you understand what documentation you’ll need before finalizing your application.

Applying in person at your local Social Security office allows face-to-face interaction and immediate problem-solving if documentation issues arise. While appointments aren’t required, scheduling one in advance typically reduces wait times and ensures you receive focused attention from staff.

Required Documents and Information

Gathering necessary documentation before starting your application prevents delays and reduces the need for follow-up submissions. Social Security requires specific documents to verify your identity, work history, and marriage/divorce status.

Essential documents include your birth certificate or other proof of birth, proof of U.S. citizenship or lawful alien status if you weren’t born in the United States, and U.S. military discharge papers if you had military service before 1968. You’ll also need W-2 forms or self-employment tax returns for the previous year to verify your own earnings record.

For divorced spouse benefit claims specifically, you must provide your final divorce decree proving the marriage ended legally. Your marriage certificate documents the marriage duration, verifying you meet the 10-year requirement. Having certified copies of these documents rather than originals often works, though Social Security may request originals for certain documents, which they’ll return to you after verification.

Bank account and routing number information for direct deposit ensures your benefits flow smoothly without payment delays. Social Security strongly encourages direct deposit for security and convenience, eliminating concerns about lost or stolen checks.

If You Don’t Have Your Ex-Spouse’s Social Security Number

While having your ex-spouse’s Social Security number streamlines the application process, it’s not absolutely required. If you don’t have this information and can’t obtain it, you can still apply by providing other identifying details about your ex-spouse.

Social Security can locate your ex-spouse’s record using their full name, date of birth, and place of birth. The more specific information you can provide, the easier it is for them to verify the correct record, particularly if your ex-spouse has a common name. Parents’ names can provide additional verification if needed.

This flexibility ensures that strained or non-existent post-divorce relationships don’t prevent you from accessing benefits you’re entitled to receive.

What to Expect During the Application Process

Processing times for divorced spouse benefit applications vary based on the complexity of your situation and current workloads at Social Security offices. Standard applications typically process within a few weeks to a few months, though complex situations requiring additional documentation or verification may take longer.

Social Security may contact you if they need additional documentation or clarification about information in your application. Responding promptly to these requests helps move your application forward without unnecessary delays.

Once approved, you’ll receive a letter confirming your benefit amount and payment start date. Your first payment typically arrives one month after your benefits begin, reflecting Social Security’s policy of paying benefits the month after they’re earned. Understanding this timing helps you plan for the initial gap between application approval and first payment receipt.

Special Situations and Common Questions

Divorced spouse benefits involve numerous nuances that can create confusion or concern. Understanding common special situations helps you navigate your specific circumstances with confidence.

If Your Ex-Spouse Hasn’t Claimed Yet

A common misconception holds that your ex-spouse must be receiving benefits before you can claim divorced spouse benefits. This isn’t accurate, though specific timing rules apply based on how long you’ve been divorced.

If you and your ex-spouse have been divorced for at least two years, you can claim divorced spouse benefits even if your ex hasn’t filed for their own retirement yet. Both you and your ex-spouse must be at least 62, and your ex-spouse must be eligible for benefits, but actual filing by your ex isn’t required. This “independently entitled divorced spouse” benefit prevents situations where an ex-spouse could block your benefits simply by not claiming their own.

If you’ve been divorced for less than two years, you generally must wait until either the two-year mark or until your ex-spouse files for their benefits, whichever comes first.

If You Remarry After Divorce

Remarriage typically ends your eligibility to claim divorced spouse benefits on your ex-spouse’s record. Once remarried, you’re treated as a current spouse for Social Security purposes, potentially eligible for benefits based on your new spouse’s work record instead.

However, if your subsequent marriage ends through death, divorce, or annulment, your eligibility to claim on your first ex-spouse’s record can be restored. Social Security recognizes that life circumstances change and provides pathways to regain benefits when new marriages don’t provide lasting financial support.

Important exceptions exist for survivor benefits, which follow different remarriage rules. If your ex-spouse dies and you remarry after age 60 (or age 50 if disabled), you can still claim divorced survivor benefits. This exception recognizes that individuals shouldn’t have to choose between companionship and financial security in their later years.

If Your Ex-Spouse Dies

The death of your ex-spouse transitions you from divorced spouse benefits to divorced surviving spouse benefits, also called divorced widow or widower benefits. These survivor benefits can be substantially larger than the spousal benefits you might have been receiving.

As a divorced surviving spouse, you can potentially receive up to 100% of what your ex-spouse was receiving (or would have been eligible to receive), compared to the 50% available through standard divorced spouse benefits. Eligibility requires that your marriage lasted at least 10 years, you’re at least 60 years old (or 50 if disabled), and you’re currently unmarried or remarried after age 60.

These survivor benefits operate under different rules than spousal benefits in several important ways. The timing of your claim relative to your full retirement age affects the benefit amount differently, and strategic considerations around when to switch from your own retirement benefit to survivor benefits require careful analysis.

If You Were Married Multiple Times

If you’ve been married multiple times with marriages lasting at least 10 years each, you have the option to claim on the record of the ex-spouse whose benefit would provide you the highest amount. Social Security doesn’t limit you to claiming on your most recent ex-spouse’s record if an earlier marriage would provide better benefits.

This flexibility allows you to optimize your benefit amount based on which ex-spouse had the strongest earnings record. You can’t receive benefits from multiple ex-spouses simultaneously, but you can choose the most advantageous option available. Social Security will help you compare these options during the application process to ensure you receive the maximum benefit you’re entitled to.

Each qualifying marriage must meet the 10-year duration requirement independently. Shorter marriages don’t count toward eligibility, and you can’t combine durations from multiple marriages to different people to meet the threshold.

If Your Ex-Spouse Remarries

Your ex-spouse’s remarriage has no impact whatsoever on your eligibility for divorced spouse benefits. Their new marriage doesn’t reduce your benefit amount, change your eligibility status, or affect your ability to claim. Social Security treats your claim as independent of your ex-spouse’s current marital status.

This independence extends to their new spouse’s benefits as well. If your ex-spouse remarries and their new spouse becomes eligible for spousal benefits, those benefits aren’t reduced by your divorced spouse benefit. Social Security can pay full spousal benefits to a current spouse while simultaneously paying full divorced spouse benefits to one or more ex-spouses from qualifying marriages.

Understanding this independence can eliminate concerns about your claim affecting your ex-spouse’s new life or relationships. The benefits you’re entitled to reflect your past partnership and the economic interdependence that developed during your marriage, independent of what happens after the divorce.

Maximizing Your Social Security Strategy After Divorce

Developing a comprehensive approach to Social Security benefits after divorce requires considering multiple factors simultaneously. Strategic thinking about timing, coordination, and long-term planning helps optimize your financial security throughout retirement.

Coordinating With Your Own Retirement Benefits

The interaction between your own retirement benefit and divorced spouse benefits creates optimization opportunities that require careful analysis. Understanding how these benefits coordinate helps you develop the most effective claiming strategy for your specific situation.

If your own benefit is currently lower than the divorced spouse benefit but growing through continued work, timing your claim strategically can maximize lifetime income. Delaying your own benefit while potentially claiming the divorced spouse benefit at full retirement age might provide optimal cash flow if your own benefit will eventually exceed 50% of your ex-spouse’s primary insurance amount through delayed retirement credits.

Alternatively, if your own benefit already exceeds the divorced spouse benefit, you’ll automatically receive your own higher amount. In this scenario, understanding that the divorced spouse option exists but doesn’t provide value helps you focus planning efforts on optimizing your own benefit claiming timing.

Tax Implications to Consider

Social Security benefits, including divorced spouse benefits, may be subject to federal income taxation depending on your total income. Understanding these tax implications helps you plan for net after-tax income rather than focusing solely on gross benefit amounts.

If your combined income (adjusted gross income plus nontaxable interest plus half of your Social Security benefits) exceeds certain thresholds, a portion of your benefits becomes taxable. For individual filers, these thresholds begin at $25,000 in combined income, with up to 50% of benefits potentially taxable between $25,000 and $34,000, and up to 85% potentially taxable above $34,000. Married couples filing jointly face similar structures with higher thresholds.

State tax treatment of Social Security benefits varies significantly, with some states fully exempting benefits from taxation while others follow federal rules or implement their own taxation schemes. Understanding your specific state’s approach helps you plan for total tax liability and net retirement income. These tax considerations affect the relative attractiveness of different claiming strategies, particularly when comparing early claiming with reduced gross benefits versus delayed claiming with higher gross benefits subject to taxation.

When Professional Guidance Makes Sense

While Social Security benefit rules are publicly available and Social Security provides assistance with applications, certain situations benefit significantly from professional financial guidance. Understanding when to seek expert help can prevent costly mistakes and optimize your long-term financial security.

Complex situations involving multiple ex-spouses, substantial pension income subject to Government Pension Offset, or significant assets that affect tax treatment of benefits warrant professional analysis. The interaction between Social Security claiming decisions and broader retirement income planning, including withdrawal strategies from retirement accounts and pension timing, creates layers of complexity where expertise provides clear value.

Emotional factors also suggest value in professional guidance. Divorce creates decision-making blind spots where stress and overwhelm impair judgment about permanent financial choices. Even Path recognizes that divorce-informed financial guidance addresses these emotional patterns without judgment.

The permanent nature of Social Security claiming decisions makes clarity particularly valuable. Once you claim benefits, especially before full retirement age, the reduction lasts for life. Professional guidance helps ensure you understand the full implications of timing decisions before making choices that can’t be reversed.

5 Common Social Security Mistakes Divorced Individuals Make

Avoiding these frequent errors can save thousands of dollars over the course of your retirement and prevent stress from reversible mistakes.

Assuming the 10-year rule is completely rigid. While marriages shorter than 10 years typically don’t qualify, Social Security may combine periods if you remarried the same ex-spouse continuously. Understanding these nuances prevents giving up on benefits prematurely.

Believing remarriage always permanently ends eligibility. While remarriage typically ends divorced spouse benefits, if your new marriage ends by death, divorce, or annulment, eligibility can be restored. Survivor benefit rules also include exceptions for remarriage after age 60.

Waiting for your ex to file when you’ve been divorced over two years. Many eligible individuals unnecessarily delay claiming because they believe their ex must file first. The two-year rule provides independence from your ex’s decisions.

Claiming early without analyzing breakeven points. The permanent reduction from early claiming often costs more in lifetime benefits than the extra years of earlier payments provide, particularly if you have average or better life expectancy.

Overlooking Government Pension Offset impacts. Government pensions from jobs not covered by Social Security can substantially reduce or eliminate divorced spouse benefits, making advance planning essential for accurate retirement income projections.

These mistakes share a common thread: permanent decisions made without complete information or emotional clarity. Professional financial guidance helps identify and avoid these errors before they become costly realities.

Conclusion

Navigating social security spousal benefits divorce rules requires balancing technical complexity with emotionally charged decision-making during an already stressful life transition. The permanent nature of claiming age decisions means rushing through these choices without full understanding can cost thousands of dollars in lifetime benefits and create financial stress that lasts throughout retirement.

Divorced spouse benefits exist specifically to provide financial stability after significant marriages end. The economic profile shows that 39% of divorced spousal beneficiaries aged 62 or older are in the lowest lifetime earnings quintile, reflecting the protective purpose these benefits serve for economically vulnerable individuals. Understanding your eligibility, calculating realistic benefit amounts, and strategically timing your claim helps optimize this important component of retirement income.

The complexity of coordinating divorced spouse benefits with your own work record, potential survivor benefits, tax implications, and broader retirement planning suggests clear value in seeking professional guidance. When the decisions affect decades of financial security, clarity matters more than speed.

Take the time to gather information about your specific situation, understand the trade-offs involved in different claiming strategies, and make decisions from a place of calm understanding rather than stress-driven urgency. Your retirement security deserves the careful consideration that comes from thorough analysis and expert guidance tailored to your unique circumstances. Talk to us at Even Pathway to discuss the best approach and get the clarity you deserve.