Divorce changes everything about how you manage money. Those joint accounts, shared bills, and combined income you once relied on? They disappear overnight, replaced by a financial reality that feels unfamiliar and often overwhelming. Whether you’re navigating a $15,000 divorce settlement or facing costs exceeding $100,000, the immediate aftermath demands clear thinking about your new financial foundation.

Starting over after divorce isn’t just about splitting assets. It’s about rebuilding an entirely new relationship with money as an individual rather than as part of a couple. With the right approach to post-divorce financial planning, you can create stability, security, and growth in this next chapter.

Guidance That Helps You Think Clearly Before Making Permanent Decisions

Even Path is a fiduciary financial guidance firm specializing in the emotionally complex financial transitions that follow divorce. When the stakes are high and the decisions are permanent, clarity matters more than speed. Schedule a conversation to begin with a clear picture of where you stand.

TL;DR: Rebuilding Finances After Divorce

Rebuilding finances after divorce requires more than separating accounts or reworking your budget. It calls for an honest assessment of your new financial reality, a plan for managing debt and rebuilding retirement savings, and the clarity to make irreversible decisions without pressure. The first year involves immediate administrative tasks, avoiding common and costly mistakes, and recalibrating retirement expectations for a single-income future. Professional fiduciary guidance, especially from advisors who understand divorce-specific financial dynamics, can mean the difference between financial recovery and years of unnecessary setback.

Key Points

- Know your new baseline. Document all assets, debts, and monthly income before making any major financial decisions.

- Underestimating costs is the most common first-year mistake. Duplicated housing, insurance, and childcare expenses catch many people off guard.

- Tax implications matter in every asset division. After-tax values, not face values, determine what you actually kept.

- Keeping the family home is often the wrong decision. Housing costs as a single income can quickly exceed what is sustainable.

- Credit rebuilding is active work. Joint debts remain your legal obligation regardless of what your divorce decree states.

- Retirement gaps are real and require a plan. Divorced retirees hold significantly lower savings balances; catch-up contributions and revised projections are essential.

- Even Path approaches divorce financial planning differently. As a fiduciary firm, Even Path is legally obligated to act in your best interest, with no product sales and no conflicts of interest.

- Professional guidance changes outcomes. 54% of divorced individuals face substantially more financial responsibility post-divorce; a structured plan dramatically reduces costly errors.

Table of Contents

Toggle

Understanding Your New Financial Reality After Divorce

The Immediate Financial Impact of Divorce

The financial shock of divorce hits differently depending on your circumstances, but it hits everyone. Recent data shows women saw a 9% income decline while men experienced 17% drops, with some men in their 30s facing declines up to 40%. For families with children, nearly 50% of non-poor families experience income reductions up to 50%, with many dropping from the 57th to 36th income percentile.

The poverty risk disparity is stark: 27% of recently divorced women have household incomes under $25,000 annually, compared to 17% of divorced men. What was once one household with shared utilities, rent, and groceries becomes two separate households. Housing costs double, moving expenses pile up, potential refinancing fees hit you, and lost economies of scale add up quickly.

Shifting from Joint to Individual Financial Management

The psychological shift from “we” to “me” in financial decision-making creates its own challenges. You’re no longer making spending decisions with a partner or balancing competing priorities through compromise. Every financial choice sits entirely on your shoulders.

This independence brings both freedom and responsibility. You gain complete control over your financial priorities and spending patterns, but you lose the safety net of dual incomes and shared financial burdens. Many people find themselves questioning decisions they made confidently as part of a couple: Can you really afford that apartment? Should you keep the car with the payment? These questions demand honest answers based on your individual financial capacity, not what worked for your former household.

Taking Stock: Assessing Your Post-Divorce Financial Situation

Documenting Your Assets, Debts, and Income

Before you can plan forward, you need a clear snapshot of where you stand financially. Create a comprehensive inventory of everything you own and owe. Gather bank statements, investment account summaries, retirement account balances, property valuations, vehicle titles, and any other assets that came to you through the divorce settlement.

Your debt picture requires equal attention. List every obligation: credit cards, student loans, car payments, personal loans, and any shared debts that remain your responsibility. Understanding which debts are solely yours versus which remain joint obligations helps you prioritize repayment strategies and protect your credit.

Calculate your new monthly income from all sources: salary, alimony, child support, investment returns, and any side income streams. This baseline number drives every financial decision you’ll make going forward.

Understanding Your Divorce Settlement’s Financial Implications

Your divorce settlement paperwork contains crucial details that shape your financial future. Asset divisions through Qualified Domestic Relations Orders (QDROs) can split retirement accounts like 401(k)s and IRAs without triggering immediate taxes or penalties, but you need to understand how these divisions affect your long-term retirement planning.

Alimony or spousal support arrangements directly impact your monthly cash flow, whether you’re paying or receiving. Child support obligations create predictable expenses that must fit within your budget framework. Property settlements might leave you with valuable assets but also maintenance responsibilities and potential tax implications when you eventually sell.

Review these arrangements carefully. Some divorces include provisions for refinancing shared debts, selling jointly owned property, or dividing business assets. Each piece carries both immediate and long-term consequences for your financial stability.

Identifying Your New Monthly Cash Flow

Cash flow becomes your most important metric post-divorce. Calculate the difference between your total monthly income and your essential expenses. This number tells you whether you’re operating with a surplus you can save and invest, or a deficit requiring immediate attention.

Track your actual spending for at least one month after separation. Many people discover their spending patterns shift dramatically as they adjust to single life. Increased costs for convenience services, childcare, or household maintenance previously shared with an ex-partner often catch people off guard.

Understanding your cash flow helps you make realistic decisions about housing, transportation, and lifestyle choices. It also reveals where you have flexibility to cut back if needed, or room to increase savings and investment contributions if your income exceeds expenses.

Not Sure What Your Numbers Actually Mean?

Even Path helps clients translate the paperwork of divorce into a clear picture of what they actually have, what they owe, and what they need to do next. Explore the Even Path process to see how we approach these transitions.

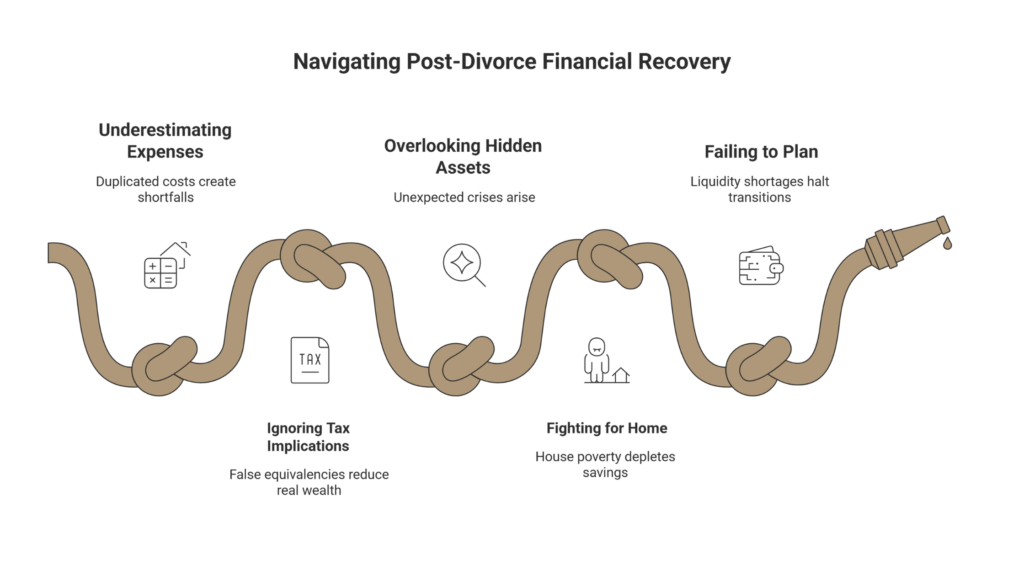

The 5 Most Costly Financial Mistakes in Year One

Financial advisors and Certified Divorce Financial Analysts consistently identify five critical errors that derail post-divorce recovery. Avoiding these mistakes protects your financial foundation during the most vulnerable transition period.

Mistake #1: Underestimating Post-Divorce Living Expenses

People fail to account for duplicated costs like separate housing, utilities, insurance, and child-related fees such as sports or tutoring. Many assume shared marital expenses will continue at similar levels, creating immediate budget shortfalls.

Consequences: Budget gaps force lifestyle cuts, credit reliance, or inability to cover essentials within months, eroding financial stability.

How to avoid it: Build a detailed budget accounting for ALL duplicated expenses before finalizing your settlement. Add a 15-20% cushion for costs you haven’t anticipated. Track spending rigorously during the first 90 days to identify gaps between projected and actual expenses.

Mistake #2: Ignoring Tax Implications of Asset Division

Dividing assets without considering after-tax values creates false equivalencies. Taking illiquid retirement accounts like IRAs over cash savings, or overlooking capital gains on investments versus property taxes on the home, reduces your real wealth substantially.

Consequences: A $50,000 IRA nets significantly less after taxes than $50,000 in cash, higher tax brackets, or surprise liabilities that strain cash flow in the first year.

How to avoid it: Calculate after-tax values of all assets during settlement negotiations. A $100,000 traditional IRA might equal only $70,000 after taxes, while $100,000 in a Roth IRA or cash represents its full value. Consult a tax professional or CDFA before finalizing divisions.

Mistake #3: Overlooking Hidden Assets and Debts

Missing undisclosed accounts like forgotten PayPal balances, cryptocurrency holdings, or joint debts that persist post-divorce creates unexpected financial crises. Credit cards with both names remain your legal obligation regardless of divorce decree language assigning them to your ex-spouse.

Consequences: Unexpected liabilities hit credit scores, lead to collections, or force repayment of an ex-spouse’s debts.

How to avoid it: Pull credit reports from all three bureaus during divorce proceedings. Review every account, subscription, and recurring charge. Document joint debts and close or separate them immediately after settlement. Monitor credit quarterly for two years post-divorce to catch issues early.

Mistake #4: Fighting to Keep the Family Home

Insisting on retaining the house for emotional or child stability reasons without budgeting for solo mortgage, taxes, maintenance, and utilities creates what financial advisors call “house poverty.”

Consequences: High costs deplete savings within 12 months, create foreclosure risk, or force eventual sale under financial duress rather than on your terms.

Decision framework for keeping your home:

- Calculate total housing costs: mortgage + property taxes + insurance + maintenance + utilities

- Divide by your gross monthly income

- If the result exceeds 28%, you likely cannot afford the home long-term as a single income

- Factor in one-time costs: refinancing fees, buying out your ex’s equity, repairs needed

- Consider opportunity cost: Could selling and downsizing free up equity for emergency funds or debt elimination?

Mistake #5: Failing to Plan for Ongoing Expenses

Not budgeting for liquidity needs like legal fees, moving costs, furniture, or future expenses like children’s braces, college, healthcare inflation, or support insurance gaps creates compounding stress.

Consequences: Liquidity shortages halt transitions, spark conflicts over uncovered children’s expenses, or derail retirement savings.

How to avoid it: Create a 12-month expense projection including one-time costs and anticipated changes. Build a separate “transition fund” covering moving, deposits, furniture, and initial setup costs before spending on discretionary items. Maintain detailed records of child-related expenses and establish clear communication systems with your co-parent about cost-sharing.

Essential Administrative Tasks for Financial Independence

Separating Accounts and Updating Financial Institutions

Your first administrative priority is establishing complete financial separation. Open individual checking and savings accounts in your name only. Transfer your portion of joint account balances based on your settlement agreement, then close those joint accounts entirely to prevent future complications.

Contact every financial institution where you held joint accounts and provide necessary documentation to remove your ex-spouse from accounts you’re retaining individually. Update addresses, phone numbers, and email contacts to ensure all financial communications come directly to you. This separation protects you from potential financial decisions your ex-spouse might make that could affect your credit or create unexpected liabilities.

Closing or Removing Names from Joint Credit Accounts

Joint credit accounts represent significant risk after divorce. Even if your divorce decree assigns certain debts to your ex-spouse, creditors can still pursue you for payment if your name remains on the account.

For larger debts like mortgages or auto loans, removal typically requires refinancing in one person’s name alone. You can learn more about how alimony and support arrangements interact with debt to understand the full scope of ongoing financial obligations.

Updating Beneficiaries, Estate Documents, and Insurance Policies

Life insurance policies, retirement accounts, investment accounts, and bank accounts all contain beneficiary designations that likely list your ex-spouse. These designations typically supersede your will, so updating them immediately after divorce finalizes is essential.

Your estate planning documents require thorough revision. Update your will to reflect new wishes for asset distribution. Revise your power of attorney designations for both healthcare and financial decisions. Insurance policies need attention beyond beneficiary updates, including obtaining your own health insurance if you were previously covered under your spouse’s plan.

Creating a Realistic Post-Divorce Budget

Calculating Your New Income and Fixed Expenses

Budgeting after divorce starts with hard math. List every dollar coming in, then list your fixed expenses that remain constant each month regardless of your choices: rent or mortgage, car payments, insurance premiums, minimum debt payments, and utility base charges.

The gap between income and fixed expenses reveals your financial flexibility. If fixed expenses consume most or all of your income, you’re operating on the edge with no room for unexpected costs or savings. This situation demands either income increases or difficult decisions about reducing fixed costs through moves, vehicle changes, or lifestyle adjustments.

Identifying Areas to Reduce Spending Without Sacrificing Stability

Look for expense categories where you can trim without creating hardship. Subscription services often accumulate unnoticed: streaming platforms, apps, memberships you rarely use. A monthly audit might reveal $100 or more in charges you won’t miss if you cancel them.

Housing represents the largest expense and potentially the biggest opportunity for savings. Could you downsize to a less expensive apartment? Would moving to a more affordable neighborhood make sense? Could taking on a roommate help bridge a temporary income gap? These decisions carry real tradeoffs, but they might provide breathing room during financial recovery.

Transportation costs offer another potential savings area. If you’re maintaining two vehicles after divorce, can you comfortably afford both? Would selling one vehicle and using rideshare services for occasional needs actually cost less?

Building Flexibility Into Your Budget for Unexpected Costs

Post-divorce life brings unexpected expenses. Create spending categories with built-in cushions. If your average grocery bill runs $400 monthly, budget $450. If your car typically needs $100 in gas, allocate $125. These small buffers add up to create breathing room when life happens.

Consider using a zero-based budgeting approach where every dollar gets assigned a job, including dollars assigned to “miscellaneous” or “unexpected expenses.” This method ensures you’re not accidentally overspending in variable categories while maintaining flexibility for surprises.

Managing and Recovering from Divorce-Related Debt

Prioritizing Debt Repayment: High-Interest vs. Strategic Obligations

Divorce often leaves you with debt. Survey data shows 42% of divorced individuals reported credit card debt as a factor in their divorce, with many taking on additional debt post-divorce ranging from under $1,000 to over $25,000.

Prioritize high-interest debt first. Credit cards charging 18% to 25% interest drain your financial resources faster than almost any other obligation. Focus extra payments on these balances while maintaining minimum payments on everything else. This “avalanche method” saves the most money over time.

However, some debts deserve strategic handling beyond pure math. A car loan enabling you to get to work holds different importance than discretionary credit card debt. Student loans often offer flexible repayment options and tax advantages that make aggressive early repayment less urgent than high-interest consumer debt.

Understanding How Divorce Impacts Your Credit Score

Divorce itself doesn’t directly appear on credit reports, but the financial behaviors surrounding divorce certainly do. Over half of divorced individuals experienced credit score decreases of 50+ points after divorce, driven by factors like missed payments, high credit utilization, and closed accounts.

Joint accounts create particular credit risks. If your ex-spouse misses payments on debts with your name attached, those late payments hurt your credit score even if your divorce decree assigns the debt to them. Credit utilization often spikes after divorce when you’re suddenly relying more heavily on credit cards to cover expenses while adjusting to reduced income.

Rebuilding Credit as a Single Individual

Recovering financially after divorce requires intentional credit rebuilding. Start by establishing individual credit accounts if you relied primarily on joint accounts during marriage. A credit card in your name alone, even with a modest credit limit, begins building your independent credit history.

Pay every bill on time, every time. Payment history represents the largest factor in credit scoring, and consistent on-time payments gradually repair damage from the divorce period. Set up automatic minimum payments if needed to prevent missed due dates during this transitional period.

Monitor your credit reports quarterly through the free annual reports available from each bureau. Dispute any errors immediately, particularly accounts showing as joint that should reflect your individual status after divorce.

Rebuilding Your Emergency Fund and Savings

Setting Achievable Savings Goals for Your New Situation

Post-divorce financial planning demands a rebuilt safety net. Financial experts generally recommend emergency funds covering three to six months of essential expenses for single-income households, acknowledging the increased vulnerability when you don’t have a second income to fall back on during crises.

If saving three to six months of expenses feels overwhelming, start smaller. A $500 to $1,000 starter emergency fund provides enough cushion for common unexpected expenses like car repairs or medical copays. Calculate your actual emergency fund target based on your essential monthly expenses. If you spend $3,000 monthly on necessities, a three-month fund requires $9,000. Breaking it into monthly savings targets of $200 gets you there in under four years.

Automating Savings to Ensure Consistent Progress

Automation removes willpower from the savings equation. Set up automatic transfers from checking to savings accounts on the day after each paycheck arrives. This “pay yourself first” approach ensures savings happen before discretionary spending can consume available funds.

Many employers offer direct deposit split options, automatically routing a percentage of each paycheck to savings before money hits your primary checking account. Financial apps and online banking platforms often include features that round up purchases to the nearest dollar and transfer the difference to savings, helping emergency funds grow incrementally through everyday spending.

Where to Keep Emergency Funds for Accessibility and Growth

Emergency funds need to balance accessibility with growth. High-yield savings accounts at online banks currently offer substantially higher interest rates than traditional brick-and-mortar banks, often 4% to 5% versus 0.01% or less.

Money market accounts provide another option, typically offering competitive interest rates with check-writing privileges for easy access. Avoid keeping emergency funds in investment accounts where market volatility could reduce your balance exactly when you need the money. The purpose of an emergency fund is immediate availability when life surprises you, not maximum returns.

Adjusting Your Retirement Planning After Divorce

Assessing How Divorce Affected Your Retirement Accounts

Divorce often devastates retirement planning. Data shows divorced retirees have significantly lower 401(k) and savings balances, with married retirees holding over $100,000 more than their divorced counterparts. This gap reflects asset divisions that split decades of accumulated retirement savings.

Review every retirement account you own: 401(k)s, IRAs, Roth IRAs, pensions, and any other tax-advantaged retirement vehicles. Understand exactly what you retained after the divorce settlement and what was transferred to your ex-spouse through QDROs or other legal mechanisms.

Calculate how the asset split affects your projected retirement income. Divorced retirees average $1,940 monthly from pensions, Social Security, and accounts, compared to $2,577 for married retirees (a difference that compounds over decades of retirement).

Recalculating Retirement Needs as a Single Person

Your retirement expense assumptions need updating for single-person living. Some costs decrease: you’re feeding one person, not two, and might need less living space. Other costs remain constant or increase, particularly healthcare and housing maintenance expenses you previously shared.

Estimate your retirement expenses based on your current lifestyle and anticipated changes. Housing, healthcare, food, transportation, insurance, taxes, and discretionary spending all factor into your retirement budget. Multiply your annual expense projection by 25 to estimate a minimum retirement savings target using the 4% withdrawal rule.

If your recalculated target exceeds your current trajectory, you have options: increase contributions, delay retirement, develop additional income streams, or adjust your retirement lifestyle expectations.

Maximizing Contributions and Catch-Up Opportunities in 2026

Aggressive retirement saving becomes essential after divorce, particularly if you are over 50 and eligible for catch-up contributions. These provisions allow higher annual contributions to 401(k)s and IRAs beyond standard limits, helping you rebuild retirement balances faster.

Maximize your 401(k) contributions, especially if your employer offers matching funds. Employer matches represent free money that accelerates your recovery. Consider Roth IRA contributions or Roth conversions as part of your strategy. Roth accounts offer tax-free withdrawals in retirement, providing tax diversification alongside traditional pre-tax retirement accounts. Evaluate your investment allocation carefully. Divorce often occurs in middle age, when you may have decades until retirement. Avoid shifting too conservatively out of emotional reaction to the transition.

Pre-Retirement Anxiety Is Common After Divorce. You Are Not Alone.

Many people navigating divorce in or near retirement carry a specific kind of financial anxiety: the fear that the divorce has permanently derailed their plans. Even Path has worked with clients in exactly this position. Read more about managing pre-retirement anxiety or connect directly with our team to build a realistic path forward.

Increasing Income and Career Considerations

Evaluating Your Current Income and Career Path

Financial recovery after divorce often requires earning more, not just spending less. Honestly assess your current income against your needs and goals. Are you earning what you’re worth based on your skills and experience? Does your current role offer advancement potential, or have you plateaued?

Research salary ranges for your position and experience level in your geographic area. Comparison sites and industry reports provide benchmarks for whether you’re underpaid relative to market rates. Consider whether career changes might serve your financial recovery. Could pivoting to a higher-paying industry or role make sense?

Strategies for Negotiating Raises or Pursuing Advancement

If you’re currently employed, pursuing a raise or promotion might offer the fastest path to increased income. Document your achievements, contributions, and value to your organization. Research market rates for your position to support your negotiation with concrete data.

Schedule a meeting with your manager specifically to discuss compensation and advancement opportunities. Present your case confidently, emphasizing results you’ve delivered and the value you bring. Advancement sometimes means changing employers rather than waiting for internal opportunities. Job switching typically delivers larger percentage increases than staying with the same organization.

Exploring Side Income or Skill Development Opportunities

Side income can accelerate financial recovery while maintaining the stability of your primary employment. Consider skills you already possess that others might pay for: consulting, freelance work, tutoring, or specialized services aligned with your professional expertise.

Digital platforms make it easier than ever to monetize skills and knowledge. Freelancing platforms connect skilled professionals with clients globally. Online teaching platforms need subject matter experts.

Skill development investments might pay dividends through career advancement or new income streams. Certifications, advanced degrees, or specialized training programs require upfront time and money but can substantially increase earning potential. Evaluate these opportunities based on realistic income projections and payback timelines.

Planning for Children’s Financial Needs Post-Divorce

Managing Child Support and Co-Parenting Expenses

Child support provides essential income for custodial parents or represents a significant expense for non-custodial parents. Understanding your obligations or entitlements clearly helps with accurate budgeting and financial planning. In fiscal year 2024, $29.5 billion in child support was collected and distributed nationally, with 97% going directly to families.

Document all child-related expenses carefully, particularly costs beyond basic child support like extracurricular activities, school supplies, medical expenses, and childcare. Many divorce agreements split these additional costs between parents, requiring clear tracking and communication to ensure proper reimbursement.

Co-parenting financial arrangements work best with clear systems. Some divorced parents use shared expense tracking apps that record costs, calculate splits based on their agreement, and facilitate reimbursement.

Balancing College Savings with Your Own Financial Recovery

College savings creates tension for divorced parents rebuilding finances. You want to provide for your children’s education while simultaneously addressing your own financial stability and retirement preparation. This balance requires honest assessment of what’s realistically achievable.

Evaluate existing college savings plans like 529 accounts that survived the divorce. Understand how these accounts were divided and what ongoing contribution obligations might exist in your divorce agreement.

Prioritize your own financial stability before aggressive college savings. Your children can borrow for college through federal student loans while you can’t borrow for retirement. Securing your emergency fund, managing debt, and building retirement savings creates a foundation that benefits your entire family long-term.

When you can contribute to college savings, even modest regular contributions compound significantly over time. A $100 monthly contribution from when a child is 8 years old until 18 grows to over $15,000 with conservative 5% returns.

When to Seek Professional Financial Guidance

Signs You Need a Financial Advisor or Planner

Complex asset divisions involving businesses, investment portfolios, or substantial real estate holdings benefit from specialized analysis that prevents costly errors. If your divorce settlement includes pensions, stock options, or other sophisticated assets, professional guidance helps optimize tax implications and division strategies.

Substantial lifestyle changes signal another opportunity for professional help. If you’re transitioning from dual income to single income with significant expense changes, a financial advisor can help model different scenarios and create sustainable long-term plans. Survey data reveals 40% of divorced individuals report derailed retirement plans, with 54% facing substantially more financial responsibilities post-divorce.

Persistent financial stress, confusion, or feeling overwhelmed by your post-divorce financial situation indicates you might need help. Financial advisors provide structure, accountability, and expert guidance that reduces stress while improving outcomes.

What to Look for in Post-Divorce Financial Support

Certified Divorce Financial Analysts (CDFAs) specialize specifically in divorce-related financial planning. These professionals combine financial planning expertise with deep understanding of divorce’s unique challenges, from asset division to cash flow modeling to tax implications of different settlement options.

Certified Financial Planners (CFPs) offer comprehensive financial guidance covering all aspects of your financial life: budgeting, investments, retirement planning, insurance, and estate planning. Look for advisors who operate as fiduciaries, meaning they’re legally obligated to act in your best interests.

Interview multiple advisors before committing. Ask about their experience with divorced clients, their approach to financial planning, their fee structure, and what ongoing services they provide. The right advisor should communicate clearly, demonstrate understanding of your situation, and inspire confidence in their expertise and integrity.

5 Financial Moves to Make in the First 90 Days After Divorce

These steps are practical, actionable, and designed to protect your financial foundation before the dust fully settles.

- Open individual accounts immediately. Separate finances are not just practical; they are legally and emotionally essential.

- Pull all three credit reports. Identify joint accounts still in your name and begin the process of closing or transferring them.

- Update every beneficiary designation. Retirement accounts, life insurance, and investment accounts all need to reflect your new reality.

- Build a 90-day expense projection. Account for duplicated costs, transition expenses, and any new recurring obligations.

- Consult a fiduciary advisor. Not just for investment advice, but to map out the full financial picture before making irreversible decisions.

These five steps will not solve everything, but they create a foundation that prevents the most common and costly early mistakes.

When to Seek Professional Financial Guidance

Knowing when professional guidance adds value is itself a form of financial wisdom.

Signs You Need a Financial Advisor or Planner

Complex asset divisions involving businesses, investment portfolios, or substantial real estate holdings benefit from specialized analysis that prevents costly errors. If your divorce settlement includes pensions, stock options, or other sophisticated assets, professional guidance helps optimize tax implications and division strategies.

Substantial lifestyle changes signal another opportunity for professional help. If you are transitioning from dual income to single income with significant expense changes, a financial advisor can help model different scenarios and create sustainable long-term plans. Survey data reveals 40% of divorced individuals report derailed retirement plans, with 54% facing substantially more financial responsibilities post-divorce.

What to Look for in Post-Divorce Financial Support

Certified Divorce Financial Analysts (CDFAs) specialize specifically in divorce-related financial planning. These professionals combine financial planning expertise with deep understanding of divorce’s unique challenges, from asset division to cash flow modeling to tax implications of different settlement options.

Certified Financial Planners (CFPs) offer comprehensive financial guidance covering all aspects of your financial life: budgeting, investments, retirement planning, insurance, and estate planning. Look for advisors who operate as fiduciaries, meaning they are legally obligated to act in your best interests. Interview multiple advisors before committing. Ask about their experience with divorced clients, their approach to financial planning, their fee structure, and what ongoing services they provide.

Conclusion

Rebuilding finances after divorce is not a straight line. Setbacks happen, unexpected expenses arise, and some months feel harder than others. What matters is consistent effort, honest assessment of your situation, and a willingness to make thoughtful decisions rather than reactive ones. Every budget you stick to, every debt you eliminate, and every dollar you save represents progress toward a future you are actively building.

The financial independence and security you build through this process becomes something no future circumstances can take from you. The decisions made in the first year carry the most weight, and they deserve the most care.

Even Path is a fiduciary-first financial guidance firm built specifically for people navigating the emotionally and financially complex transitions that come with divorce, retirement, and major life changes. Unlike advisors who earn commissions from product sales, Even Path’s fiduciary obligation means every recommendation serves your interests, not a firm’s incentives. When the decisions are permanent, the guidance you receive should be, too.

Ready to Build a Clear Financial Plan for Your Next Chapter?

Even Path provides fiduciary financial guidance throughout the divorce process and beyond, helping clients in Colorado and nationally navigate asset division, retirement planning, and post-divorce financial recovery. When you are ready to move from uncertainty to clarity, schedule a conversation with Even Path. Support, structure, and a fiduciary partner in your corner.